Ten psychological traps that derail even the most disciplined investors — and how to break free from them so you can Enjoy the Ride

By Brant Wiehardt EBS CONTRIBUTOR

Sponsored article

Every investor knows the rules: buy low, sell high, diversify, stay the course. So why is it so hard to follow them? The answer, more often than not, has nothing to do with spreadsheets or stock charts. It lives between your ears.

Behavioral finance is the study of how psychological factors influence financial decisions. Over the past four decades, researchers — including Nobel laureates Daniel Kahneman and Richard Thaler — have catalogued dozens of cognitive biases that cause ordinary investors to make costly, irrational choices. The good news: once you can name a bias, you can begin to tame it.

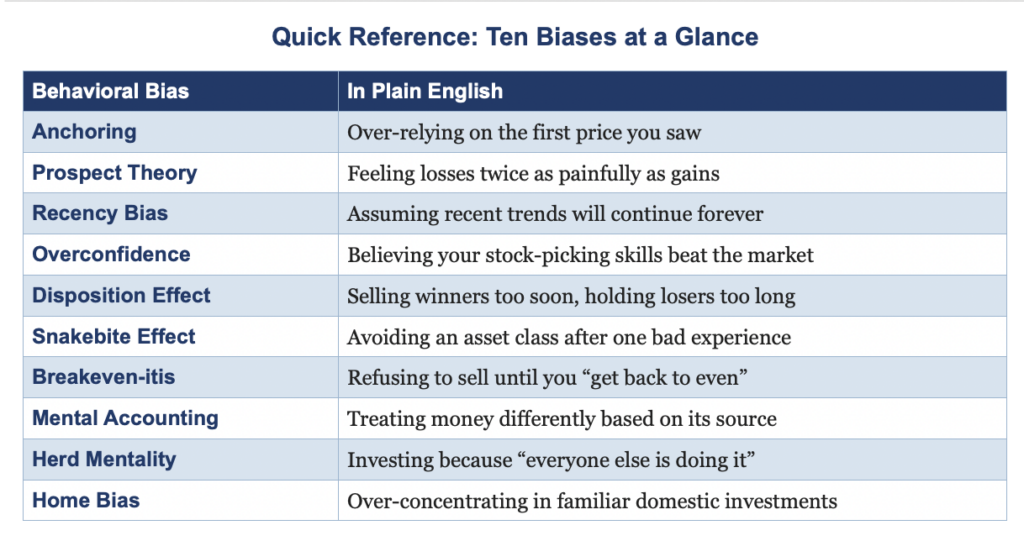

Below are ten of the most common behavioral traps, what they look like in real life, and what you can do to protect your portfolio from your own worst instincts.

“In investing, what is comfortable is rarely profitable.” — Robert Arnott

1. Anchoring

Anchoring occurs when investors fixate on a specific reference price — typically the price at which they purchased a stock — and use it as the benchmark for all future decisions, even when that number is no longer relevant to the investment’s current prospects.

Example: You bought a stock at $80. It fell to $45. Rather than evaluating the company on its current fundamentals, you refuse to sell until it “gets back to $80.” The original purchase price has become an anchor — an arbitrary number that has no bearing on whether the stock is a good investment today.

What to do: When reviewing any holding, ask yourself: “If I had $45 in cash today and no position in this stock, would I buy it?” If the answer is no, the anchor is controlling you — not sound analysis.

2. Prospect Theory

Developed by Kahneman and Tversky, Prospect Theory demonstrates that people do not weigh gains and losses symmetrically. Psychologically, losing $1,000 feels roughly twice as painful as gaining $1,000 feels pleasurable. This loss aversion distorts rational decision-making in predictable ways.

Example: An investor holds two positions — one up $5,000, one down $5,000. Prospect Theory predicts she will sell the winner to ‘lock in’ the gain (reducing the pleasure of winning) and hold the loser to avoid crystallizing the pain of a loss. Both instincts work against optimal portfolio management.

What to do: Reframe decisions in terms of total portfolio value rather than individual position gains and losses. A dollar lost and a dollar gained should carry identical weight in your analysis.

3. Recency Bias

Recency bias is the tendency to give disproportionate weight to recent events when forecasting the future. Investors experiencing a bull market begin to believe markets only go up; investors who lived through a crash expect another around every corner. Both groups are prisoners of their most recent experience.

Example: After three consecutive years of double-digit returns in a sector, retail investors pour money in — just as the cycle turns. Conversely, after a sharp correction, many investors move entirely to cash and miss the recovery. Market timing based on recent trends has a poor historical track record.

What to do: Study long-term market history, not just the last 12 months. A written investment policy statement that defines your strategy in advance can serve as an anchor against reactive decision-making.

“The investor’s chief problem — and even his worst enemy — is likely to be himself.” — Benjamin Graham

4. Overconfidence

Study after study confirms that most investors — amateur and professional alike — believe their stock-picking and market-timing abilities are above average. Statistically, this is impossible. Overconfidence leads to excessive trading, under-diversification, and the mistaken belief that one has an ‘edge’ the market has not already priced in.

Example: An investor who correctly called two market moves in a row becomes convinced she has a system. She begins concentrating her portfolio in high-conviction bets and trading more frequently. Transaction costs rise, diversification falls, and a few bad calls erase years of gains.

What to do: Track every trade, including the ones you almost made. Compare your returns — net of all fees and taxes — to a simple index fund over the same period. The data is usually humbling.

5. The Disposition Effect

The disposition effect — a term coined by researchers Shefrin and Statman — describes the well-documented tendency of investors to sell winning investments too quickly while holding onto losing ones far too long. It is, in part, an outgrowth of both anchoring and prospect theory.

Example: An investor’s portfolio holds Stock A (up 40%) and Stock B (down 35%). Wanting to “realize a win,” she sells A and holds B hoping for a rebound. In practice, this approach systematically harvests gains early and defers losses — the exact opposite of tax-efficient investing, and often of sound fundamental strategy.

What to do: Implement a disciplined rebalancing schedule. Tax-loss harvesting — strategically selling losers — is the rational inverse of the disposition effect and can add meaningful after-tax returns over time.

6. The Snakebite Effect

Like someone bitten by a snake who forever avoids the outdoors, investors who suffer a significant loss in a particular asset class often develop a lasting aversion to that entire category — even when the circumstances that caused the loss have long since changed.

Example: An investor who lost money in technology stocks during the dotcom bust avoided the sector entirely through the 2010s — missing one of the strongest decade-long rallies in market history. The snakebite was real, but the avoidance became a permanent drag on returns.

What to do: Separate the specific risk factors of a past loss from a broad asset class. Ask: has anything fundamentally changed? Valuations, business models, and market structures evolve. A prior loss is data, not a verdict.

7. Breakeven-itis

Breakeven-itis is a cousin of anchoring. It describes the psychological compulsion to hold a losing investment until it returns to the original purchase price before selling — not because the investment has merit, but because selling at a loss feels like admitting failure.

Example: An investor buys a stock at $60. It falls to $30. Rather than reassessing the investment on its current merits, she vows to hold until she is “made whole.” Meanwhile, the capital sits tied up in a poor investment rather than being redeployed into better opportunities. The market, of course, has no idea — or obligation — to return her stock to $60.

What to do: Recognize that the cost basis is irrelevant to an investment’s future prospects. The only question that matters: is this the best use of my capital today?

8. Mental Accounting

Mental accounting — another concept pioneered by Richard Thaler — describes the habit of treating money differently depending on its perceived source or intended purpose. We place money into psychological “buckets” and apply different rules to each, even though a dollar is always worth a dollar.

Example: An investor receives a $10,000 tax refund and promptly takes a vacation and buys lottery tickets — money she would never have spent so frivolously from her savings account. Similarly, investors often take outsized risks with “house money” (recent gains) that they would never take with principal.

What to do: Before making any financial decision, replace the label on the money with a simple question: “Is this the best use of $X, regardless of where it came from?” Treating all dollars as interchangeable leads to more rational allocation.

9. Herd Mentality

Humans are social animals wired to find safety in numbers. In financial markets, this instinct manifests as herd mentality — the tendency to follow the crowd into (or out of) investments, not because of independent analysis, but because “everyone is doing it.” Herding is a primary engine of asset bubbles and market panics.

Example: In the early months of 2021, retail investors piled into meme stocks and speculative assets largely because social media communities were celebrating their rise. Many bought at or near the top, following the herd — and absorbed devastating losses when sentiment reversed.

What to do: When your reason for investing is that “everyone is talking about it,” treat that as a warning, not a recommendation. Popularity and investment merit are not the same thing, and they are frequently inversely correlated.

10. Home Bias

Home bias is the tendency of investors to over-allocate to domestic stocks and bonds simply because they feel more familiar and comfortable. While patriotism is admirable, domestic familiarity is not an investment thesis. U.S. investors, for example, often hold portfolios with 80–90% domestic exposure despite the U.S. representing roughly 60% of global market capitalization.

Example: A Montana investor holds a portfolio consisting almost entirely of large U.S. companies and locally headquartered businesses. Emotionally, these feel “safe” because they are familiar. In reality, the portfolio is dangerously under-diversified across geographies, currencies, and economic cycles.

What to do: Build global diversification into your investment policy statement deliberately. International and emerging market exposure has historically provided meaningful diversification benefits — particularly during periods when U.S. markets lag. Familiarity and safety are not synonymous.

The Antidote: Process Over Emotion

Behavioral finance does not suggest that all investors are irrational all the time. It suggests that all investors are vulnerable to predictable, systematic errors — and that awareness alone is not enough to prevent them. The most effective protection is structure: a written investment plan, a disciplined rebalancing process, and — where appropriate — a trusted financial advisor who can serve as an objective sounding board when emotions run high.

Markets normally reward patience, diversification, and process. They normally punish impulsiveness, concentration, and emotion. Knowing the enemy — your own cognitive biases — is the essential first step toward investing with the clarity and discipline your financial future deserves.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett

Brant Wiehardt is a Partner and Financial Advisor at Shore to Summit Wealth Management. He currently works and lives in Bozeman, MT with his wife and children.

.Wells Fargo & Company and its affiliates do not provide legal or tax advice. This communication cannot be relied upon to avoid tax penalties. Please consult your tax and legal advisors to determine how this information may apply to your own situation. Whether any planned tax result is realized by you depends on the specific facts of your own situation at the time your tax return is filed.

This article was written by Wells Fargo Advisors Financial Network and provided courtesy of Brant Wiehardt – Associate Vice President Shore to Summit Wealth Management in Bozeman, MT at 406-219-2900.

Investment products and services are offered through Wells Fargo Advisors Financial Network, LLC (WFAFN), Member SIPC. Shore to Summit Wealth Management is a separate entity from WFAFN.

©2023 – 2026 Wells Fargo Advisors Financial Network, LLC.